Why allocate to hybrid capital instead of traditional high yield?

By Peter Doherty, Head of Fixed Income at Sanlam Investments UK

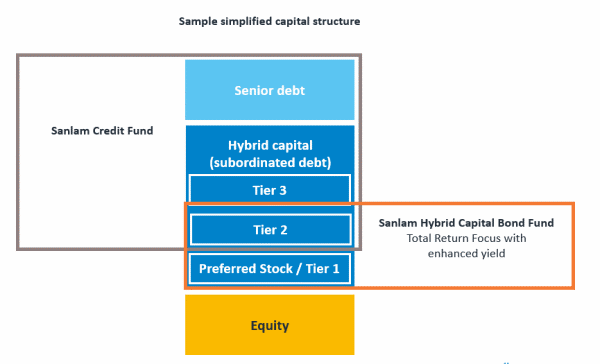

Q1. What is hybrid capital?

Hybrid capital is a generic term covering all subordinated securities that sit in the middle of a company’s balance sheet: lower ranked than senior debt but senior to equity.

Source: Sanlam Investments, April 2021.

Q2. What are the main differences between hybrid capital and high yield?

The vast majority of hybrid capital is issued by large, household name companies with an investment grade senior credit rating such as Legal & General, Lloyds Bank and British Telecom.

In contrast, traditional high yield (HY) is by definition an issue of debt by a sub-investment grade company such as Virgin Media or Pizza Express.

Q3: What sort of companies issue hybrid capital?

There’s a wide range of household names issuing hybrid securities – Legal & General and EDF are two. Lloyds Bank and Allianz are two more. These are very large, well-known and well-respected companies with good balance sheets. They aren’t fly-by-night entities. Ask yourself, what is likely to be more risky: a bond issued by a new, heavily leveraged company engaged in say US shale oil production, or a hybrid issued by a long-established entity like L&G or EDF which has a stable, established business with large and recurring cash flows? Those are the kinds of issues that we think investors should really think about.

There’s also a reputational angle here: it doesn’t look good if investment grade companies fail to meet their debt obligations, even if the specific security they’ve reneged on happens to be rated below investment grade. By contrast, if the parent company is high yield (i.e. the parent itself is ‘junk’), there’s a very clearly implied risk that it might not make good on any of its debt in the longer term.

Traditional high yield debt is issued by a very wide range of companies; the unifying theme is that the companies themselves are ‘junk’, that is they tend to be highly leveraged and thus are not considered ‘investment grade’ as defined by independent credit ratings agencies such as S&P, Moody’s or Fitch.

Q4: What have historic defaults been in hybrid capital and high yield?

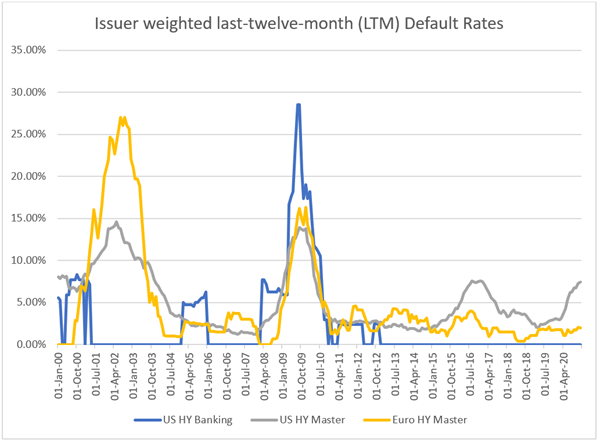

It is important to look at independent, third-party data here. If, for example, we look at data from Credit Sights, which covers the last twenty years (a period that of course includes the Global Financial Crisis – GFC) it is clear that ‘traditional’ high yield usually exhibits a higher default rate than high yield financials. (To be clear, in our fund we don’t invest in financials where the parent is high yield.)

As can be seen in the line chart below, with the exception of the GFC, default rates for high yield financials tend to be lower than they are for ‘mainstream’ high yield, and there have been long periods when HY bank defaults have been zero, which isn’t the case for high yield.

Source: Credit Sights, 31 March 2021.

*Default data from 31 January 2000 to 31 December 2020.

*‘US HY Master’ and Euro HY Master depict mainstream US and European high yield default rates respectively.

For investment grade financials, defaults are so rare that Credit Sights do not maintain a time series of default rates – indeed the only US dollar investment grade default in financials in recent decades is that of Lehman Brothers in the GFC.

Q5. Why do you advocate hybrid capital over traditional high yield?

There are a few things to think about here. First, high yield debt has performed very well in recent years – so much so that the widely-used ICE Bank of America US High Yield Index now has a yield of around 4%.[1] In our opinion, it would be better to think of ‘high yield’ as a ‘medium yield’ asset class from here.

Moreover, 2021-2023 expected high yield default rates of 3-4%[2] per annum (as assessed by Fitch Ratings and S&P) will reduce the total return from this already low number. So, for high yield you’ve got a toxic mix of very low absolute levels of yield, tight spreads (i.e. rich valuations), the likelihood of an increase in defaults and rising risk-free rates in government debt markets – everything is pointing the wrong way.

In short, taking the starting point of today’s high yield market and adjusting for expected defaults, there is, realistically, only scope for very low single-digit returns, in our opinion.

We’ve explained the impact of defaults on net returns in the table below. This is a critically important consideration given that gross yields for most asset classes remain extremely low but defaults for high yield as a specific asset class are likely to rise.

Source: Sanlam Investments, April 2021.

Q6: What about the outlook for hybrid capital? Are the risks not the same? What about the expected return from here?

According to an anonymous data source, the sterling AT1 market – a proxy for hybrid capital – offers a yield to worst of 5.6% and a yield to call of 4.1%. Even in euros, a region where deposit rates are firmly in negative territory, the equivalent figures are 4.9% and 3.4%.3 On a risk-adjusted basis, we regard these as attractive yields given the extremely low probability of default.

Both markets are subject to systemic risk – i.e. both markets will sell off heavily in a crisis such as GFC, Coronavirus Mark II or some other global calamity, as would the equity markets.

However, the big difference between traditional high yield and hybrid capital issued by investment grade companies is the much lower default rate in hybrids as evidenced by the data from Credit Sights which goes all the way back to 2000 in US dollars.[4] To put this into context, there were only four years between 2000 and the end of 2020 when issuer-weighted defaults by US high yield financials exceeded those of US high yield (those years being 2005, 2008, 2009 and 2010).[5]

With hybrid capital, where the parent is investment grade the frequency of default is trivially low. Yes, there have been a very small number of high-profile defaults such as Lehman Brothers and Northern Rock, but these are incredibly rare.

The point is that the companies aren’t classified as high yield but the individual (hybrid) issues are, because they rank lower in the capital structure in the event of default. They are deemed to be ‘risky’ because of where they sit in the capital structure. This might sound like a technical point, but it’s a critically important one.

Q7: Why do you think hybrid capital of investment grade companies has defaulted much less frequently than traditional high yield?

This links to the point above, namely that the market doesn’t look kindly on investment grade parents who renege on their responsibilities to holders of their subordinated debt. However, there is a wider point here: a lot of hybrid debt is issued by financials – banks, insurers and the like.

Because of the GFC, regulators have forced banks and other financial institutions to bolster their capital and be much more conservative in their behaviour.

This is a bad story for equity investors in banks as the days of gigantic profits (and high leverage) are over, but it’s a great story for credit investors as it means you are more likely to be repaid at maturity. If anything, retail banks in particular have become much more utility-like than they were prior to the GFC – but the memory of the crisis means that they still have to offer investors some pick up in spread when they issue debt. This means it is possible to achieve attractive returns without running the default risk that is inherent in ‘traditional’ high yield. The last thing the regulators want is another banking crisis – and the changes made since the GFC mean that if we do see another crisis, the banks won’t be the source.

Q8: Aren’t bank defaults quite common?

Not at all. Bank defaults are actually rare and that’s why when they do occur, they tend to be a big deal. Investors will remember the likes of Northern Rock in the UK and Lehman Brothers in the US, but those kinds of seismic events are the exception, not the norm. In the interim, investing in bank debt and particularly hybrid debt issued by banks allows you to earn more than you could do from investing in traditional high yield with a similar volatility profile. There will always be times when the banks and the wider market experiences defaults, but there will also be periods when banks see materially fewer defaults than seen in other sectors. That’s the environment we believe we are in now.

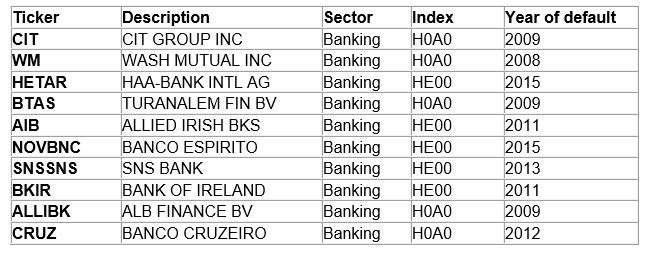

Below we’ve provided a list of the largest bank defaults from 2000 to 2020 in the US high yield index (H0A0). As you’ll see, defaults are rare (the last major one in US high yield being in 2015), and in fact these defaults make up close to 90% of the total face value of bank defaults in the index. That is to say in the high yield space they are the exception, not the norm. But again remember, we are not investing in “high yield financials” i.e. our parent company credit ratings are investment grade.

Source: CreditSights, March 2021.

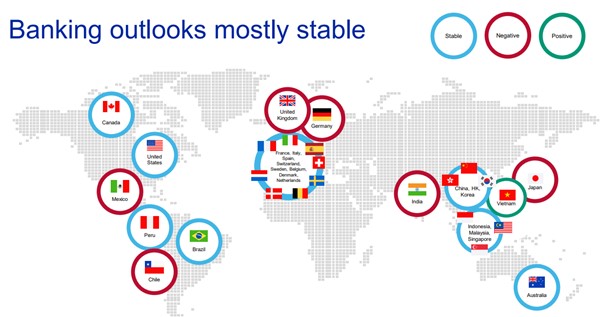

We are also encouraged that Moody’s has confirmed a ‘mostly stable’ outlook for the global banking sector, and while some economies such as the UK face a relatively slow recovery or structurally lower banking profits (Japan and Germany), one must remember that where a company is domiciled does not necessarily reflect where its key risk lie – for HSBC and Standard Chartered for example, what happens in Asia is more important than what happens here in the UK. Overall though, the picture for banks is encouraging:

Source: Moody’s, 31 March 2021.

Peter Doherty

Head of Fixed Income at Sanlam Investments UK

Watch video

In this video Peter Doherty, Head of Fixed Income at Sanlam Investments UK, gives an update on the fixed income market and makes a case for why Hybrid Capital should be considered against traditional High Yield investments.

Important Information

The fund will invest in debt securities. The government or company issuer of a bond might not be able to repay either the interest or the original loan amount and therefore default on the debt. This would affect the credit rating of the bond and, in turn, the value of the fund. Investment in bonds and other debt instruments (including related derivatives) is subject to interest rate risk. If long-term interest rates rise, the value of your shares is likely to fall. The yield is gross and could be higher than what you will receive in the future. The Fund may engage in transactions in financial derivative instruments for hedging purposes. There is a risk that losses could be made on derivative positions or that the counterparties could fail to complete on transactions. The Fund may invest in Contingent Convertible Securities (CoCo’s). The value of CoCos is unpredictable and will be influenced by many factors including, without limitation (i) the creditworthiness of the issuer and/or fluctuations in such issuer’s applicable capital ratios; (ii) supply and demand for the CoCos; (iii) general market conditions and available liquidity and (iv) economic, financial and political events that affect the issuer, its particular market or the financial markets in general. The investor may not receive a return of principal if expected on a call date or indeed at any date.

The value of this portfolio is subject to fluctuation and past performance is not necessarily a guide to future performance. The performance is calculated for the portfolio and the actual individual investor performance will differ as a result of initial fees, the actual investment date, the date of reinvestment and dividend withholding tax. All terms exclude costs. Fluctuations or movements in exchange rates may cause the value of underlying investments to go up or down.

Do remember that the value of participatory interests or the investment and the income generated from them may go down as well as up and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital. Therefore, the Manager does not provide any guarantee either with respect to the capital or the return of a portfolio. The Manager has the right to close any Portfolios to new investors to manage them more efficiently in accordance with their mandates. Collective Investment Schemes are traded at ruling prices and can engage in borrowing and scrip lending. Collective Investment Schemes (CIS) are generally medium to long term investments. A schedule of fees and charges and maximum commissions is available on request free of charge from sanlam.co.uk

Issued and approved by Sanlam Investments which is authorised and regulated by the Financial Conduct Authority. Sanlam Investments is the trading name for our two Financial Conduct Authority (FCA) regulated entities: Sanlam Investments UK Limited (FRN 459237) and Sanlam Private Investments (UK) Ltd (FRN 122588), both having its registered office at 24 Monument Street, London, EC3R 8AJ.

Tideway UCITS Fund ICAV an Irish collective asset-management vehicle registered under the laws of Ireland having its registered office at 1st Floor, 2 Grand Canal Square, Grand Canal Harbour Dublin 2, Ireland. The ICAV is an umbrella type Irish collective asset-management vehicle with segregated liability between funds incorporated under the Irish Collective Asset-management Vehicles Act 2015 of Ireland and authorised by the Central Bank of Ireland. The Fund Manager is Link Fund Solutions (Ireland) Limited a company incorporated under the laws of Ireland having its registered office at 1st Floor, 2 Grand Canal Square, Grand Canal Harbour, Dublin 2, Ireland which is authorised by the Central Bank of Ireland. Link Fund Solutions (Ireland) Limited has appointed Sanlam Investments UK Ltd as Investment Manager to this fund.

This document is provided to give an indication of the investment and does not constitute an offer/invitation to sell or buy any securities in any fund managed by us nor a solicitation to purchase securities in any company or investment product. It does not form part of any contract for the sale or purchase of any investment. The information contained in this document is for guidance only and does not constitute financial advice.

The fund price is calculated on a net asset value basis, which is the total value of all assets in the portfolio including any income and expense accruals. Trail commission and incentives may be paid and are for the account of the manager. Performance figures quoted are from Sanlam and are shown net of fees. Performance figures for periods longer than 12 months are annualized. NAV to NAV figures are used. Calculations are based on a lump sum investment.

Please note that all Sanlam Funds carry some degree of risks which may have an adverse effect on the future value of your investment. Any offering is made only pursuant to the relevant offering document, together with the current financial statements of the relevant fund, and the relevant subscription/application forms, all of which must be read in their entirety together with the Fund prospectus, the Fund supplement and the KIID. All these documents explain different types of specific risks associated with the investment portfolio of each of our products and are available free of charge from sanlam.co.uk. No offer to purchase securities will be made or accepted prior to receipt by the offeree of these documents, and the completion of all appropriate documentation. Use or rely on this information at your own risk. Independent professional financial advice should always be sought before making an investment decision as not all investments are suitable for all investors.

Sources:

[1] Source: BoAML, St Louis Fed, 29 March 2021.

[2] Source, S&P, Fitch Ratings. As at 31 March 2021.

[3] Source: Autonomous, yields quoted as at 1 March 2021. The Autonomous data herein is part of a larger body of investment analysis. For their latest research reports, which contain information that may be used to support investment decisions and appropriate disclosures, please see their website at https://www.autonomous.com. Autonomous makes no representation or warranty concerning the accuracy of any data contained herein.

[4] Source: Credit Sights. USD default rates for the period 31.01.00 to 31.12.20. See also the line chart above.

[5] Source Credit Sights, issuer weighted US HY bank defaults versus US HY Master index defaults, 31.00.2000 to 31.12.2020.

Share On:

Comments are closed.