The right intent and strategy, but it’s a battle to stabilise debt

By Arthur Kamp, chief economist

The key take-outs of Budget 2021 for South Africa and its citizens:

- The Treasury shows the right intent and strategy.

- But, the debt ratio continues to increase over the medium term.

- And, South Africa is a long way from a primary budget surplus

The good news: tax collection was not as poor as anticipated

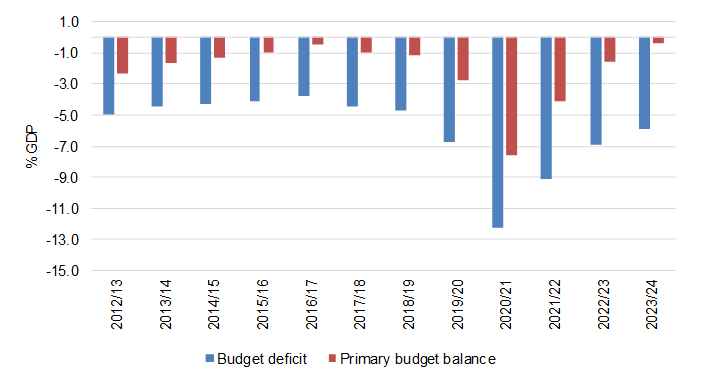

Main Budget revenue collection was R99.6 billion better in 2020/21 than at the last MTBPS projection and is expected to beat previous projections by a further R196.4 billion cumulative over the next three years. This translated into a smaller than expected budget deficit of 12.3% of GDP in 2020/21 (relative to the 2020 MTBPS projection of 14.6% of GDP) and improved projections for the budget balance over the medium term.

National Treasury is employing the right strategy

The National Treasury has also employed an appropriate strategy to address South Africa’s fiscal problems by:

- restraining consumption expenditure,

- growing capital expenditure faster than other spending categories, and

- raising indirect taxes (mitigated by compensating for fiscal drag), while refraining from increasing income taxes further.

The latter are a disincentive to saving and investment. Indeed, the Treasury signaled a cut in the corporate tax rate to 27% for companies with years of assessment starting on or after 1 April 2022.

Treasury’s projections for the 2023/24 deficit shows improvement

In the 2020 Medium Term Budget Policy Statement (MTBPS) the Main Budget primary balance (revenue less non-interest spending) was projected to decrease to -1.4% of GDP by 2023/24. The February 2021 Budget shows a decline in this deficit to -0.8% of GDP over the same period. The consolidation is achieved through an average annual decline in real non-interest spending of -0.8% on average per year over the three years. In turn, expenditure discipline, critically, hinges on constraining the increase in the consolidated government wage bill to average annual increases of just 1.2% in current prices over the medium term. However, this is onerous, implying execution risk is material.

But the debt ratio continues to deteriorate

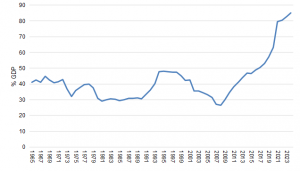

Despite the right intent from the Treasury, the fiscal challenge remains daunting. Looking forward, the Treasury projects that the gross loan debt ratio will stabilise at 88.9% of GDP in 2025/26, before declining. The revised debt trajectory is significantly flatter than its previous forecast, which showed the debt ratio increasing to 95.3% over the same period. But, the point is the debt ratio is already excessive and it continues to increase over the next five years. In any event, the improvement in the primary balance is not sufficient to stabilise the debt ratio. Given the current gap between the effective real interest on debt and the trend real growth rate of the economy, a primary balance surplus of close to 2% of GDP is required to steady the ship. That is a large swing from an expected primary balance deficit of -4.0% of GDP in 2021/22.

Government’s borrowing requirement is likely to decrease

The increase in gross loan debt is a function of the budget deficit, the discount on loan transactions, revaluation of inflation-linked bonds, revaluation of foreign currency debt and the change in cash and other balances. At end March 2021, the government’s cash balances are expected to amount to R294.6 billion, which is lower than the R378.4 billion recorded at end January 2021, but still large. A decline in cash balances of R107.9 billion, along with a decline in other balances of R4.7 billion, helps fund the government’s gross borrowing requirement of R547.9 billion in 2021/22. Accordingly, issuance of domestic long-term loans falls to R380 billion in 2021/22 from R518.5 billion in 2020/21, while issuance of short-term loans falls to R9 billion from R97.2 billion.

Graph 1: Main budget balances

Source: SA National Treasury, Sanlam

Graph 2: Gross loan debt

Source: SA National Treasury, Sanlam

That said, even though the government’s borrowing requirement is expected to decline over the next three years, it remains large. In 2020/21, including loan redemptions, the gross borrowing requirement amounted to R670.3 billion (13.6% of GDP). And, although the Main Budget balance is projected to decline to R389 billion (6.5% of GDP) in 2023/24, redemptions increase to R152.7 billion from R66.9 billion in 2020/21, leaving a gross borrowing requirement of R541.7 billion (9% of GDP) in 2023/24. Hence, the government continues to absorb a large share of domestic savings, which will continue to constrain the ability of the private sector to invest – unless foreign capital inflows are sustained at a high level.

But debt servicing costs remain high

The negative debt dynamics at work are clearly illustrated by the budgeted increase in debt servicing cost from 4.7% of GDP in 2020/21 to 5.6% of GDP in 2023/24; or from 19.4% of Main Budget revenue in 2020/21 to 22.2% of Main Budget revenue in 2023/24. This leaves fewer resources for development.

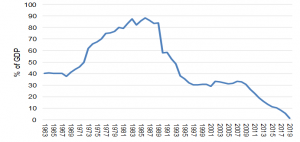

Importantly, too, although budget balances and debt ratios are key indicators, true fiscal consolidation requires an improvement in the government’s balance sheet. However, as yet, there is little indication of this as general government’s net asset value (capital stock less liabilities) has shown a persistent downward trend since the Global Financial Crisis.

Graph 3: General government net asset value

Source: SA Reserve Bank

And state-owned companies remain a liability

Meanwhile, there is also the issue of large contingent liabilities due to government guarantees on the debt of state-owned companies. These guarantees are expected to amount to R581 billion at end March 2021, with an exposure of R410.3 billion. Eskom accounts for 77.2% of the latter. In addition, medium-term debt redemptions of state-owned companies are large, amounting to a total of R182.8 billion. Hence, the deterioration in the balance sheet of public sector enterprises holds additional risk.

Ultimately, although there is some progress, the scale of the improvement required in the primary budget balance to stabilise the debt ratio against the backdrop of low potential economic growth, high real borrowing costs and a deterioration in the state’s balance sheet, implies the risk associated with South Africa’s fiscal policy remains high. As Minister Mboweni noted ‘our public finances are dangerously overstretched’.

Share On:

Comments are closed.