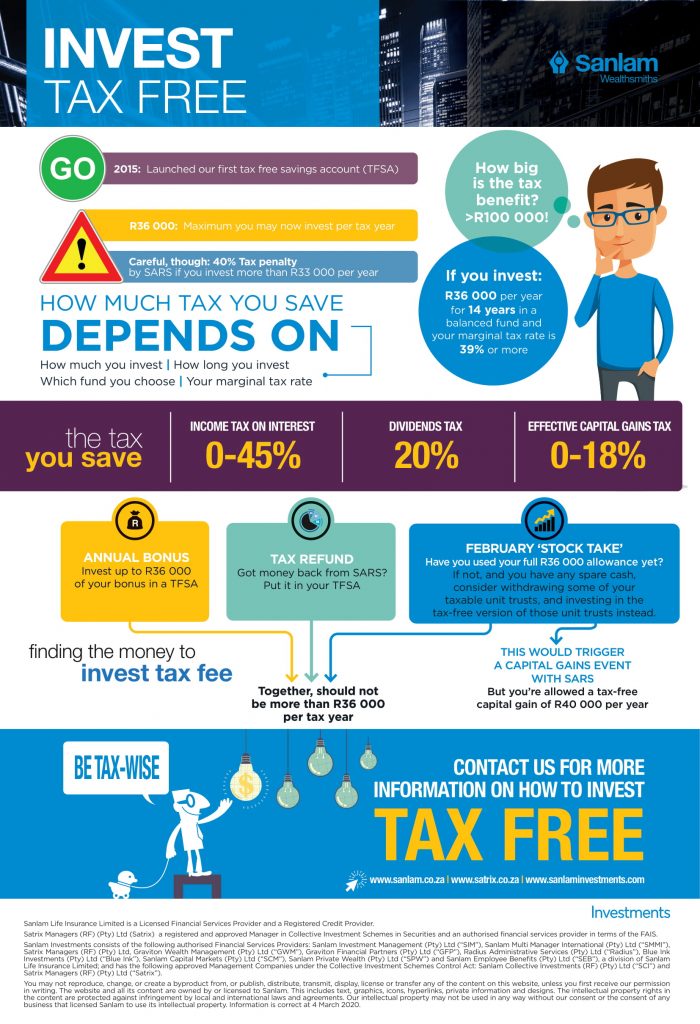

Tax-free saving: the fast facts

With the total tax burden of South Africans on the rise, it’s time to look more closely at those products that give you that much needed tax break. Retirement annuity (RAs) have been around for many years and most investors are familiar with this product, but tax-free savings accounts (TFSAs) were only introduced in 2015, and is fast gaining popularity among retail investors – for obvious reasons.

The benefits of a TFSA

All the proceeds – dividends, interest and capital gains – are tax-free. After several years of investing in a balanced or equity portfolio, the capital gain payable when ultimately withdrawing the money could be substantial. This tax benefit makes the TFSA very attractive relative to discretionary, taxable products.

The contribution limits of a TFSA

Your overall TFSA contributions are limited to R36 000 per tax year. Any contributions exceeding the annual cap will be taxed at 40% and therefore need to be monitored carefully to remain within the annual limit. You cannot roll over this year’s unused allowance to next year, so if you don’t contribute before the end of February, you’ll miss the boat for the tax year. A lifetime contribution limit of R500 000 also applies.

The tax benefits are significant compared to a taxable product

The benefit may be small during the first few years, but as the value of the investment grows, it becomes significant. The difference between investing R3 000 per month (R36 000 per year) in a balanced portfolio TFSA earning 10% p.a. and investing the same amount in a ‘normal’ taxable product earning 10% p.a. before tax over a period of 15-16 years could result in several hundred thousand rand more in your pocket. If you’re in the 39% tax bracket you’ll save more than R100 000 in today’s terms. But the longer you invest in this balanced fund TFSA and the higher your marginal tax rate, the more tax you’ll save.

You’ll be pleasantly surprised at the superior annual returns of tax-free investments compared to their standard, taxable counterparts, particularly for pure equity and high equity funds. Not paying any dividends tax now and no capital gains tax in future will make a dramatic difference to your pocket. So, make sure to not miss another tax year for planting the seeds for a tax-free harvest in future.

Share On:

Comments are closed.