In uncharted territory

By Melville du Plessis, portfolio manager at Sanlam Investment Management

The world is currently in uncharted territory, as many keep highlighting. But this will always be the case as we move forward through time. The fiscal and monetary policy responses to the 2007 to 2008 global financial crisis were on an unprecedented scale – with fiscal stimulus and budget deficits leading to an increase in debt levels worldwide. On the other hand interest rates are still at their lowest levels in history and quantitative easing policies have led to massive expansions of central bank balance sheets. However, there seems to be no comparable response to the “Geopolitical Recession” the world is currently in.

One of the challenges investors are facing is extraordinary global debt dynamics. Let’s explore this phenomenon a bit further.

An exceptional bull run in bonds

Global bond yields have been grinding lower for the last 35 years. It has been one of the longest bull runs in history with total returns from global bonds over the last few decades comparable to equity market returns – and at times even beating them for extended periods. The returns investors have seen in global developed market bonds cannot be expected again. And with interest rates at such low levels it is difficult to see how this will turn out to be a good investment years ahead.

Many have even questioned whether a bond bubble is looming as a result of central bank policies as well as their associated effects and unintended consequences: low interest rate policies may have spilled over into other asset classes leading to overinflated prices elsewhere. We have reached a point in history where some debt instruments even carry negative interest rates. This is counterintuitive: you actually have to pay someone to lend them money! During the last few years the amount of negative yielding debt increased significantly with the total amount peaking at around $13 trillion during the second half of 2016. It is a staggering amount and the thought of negative yielding securities on this scale was previously inconceivable by many.

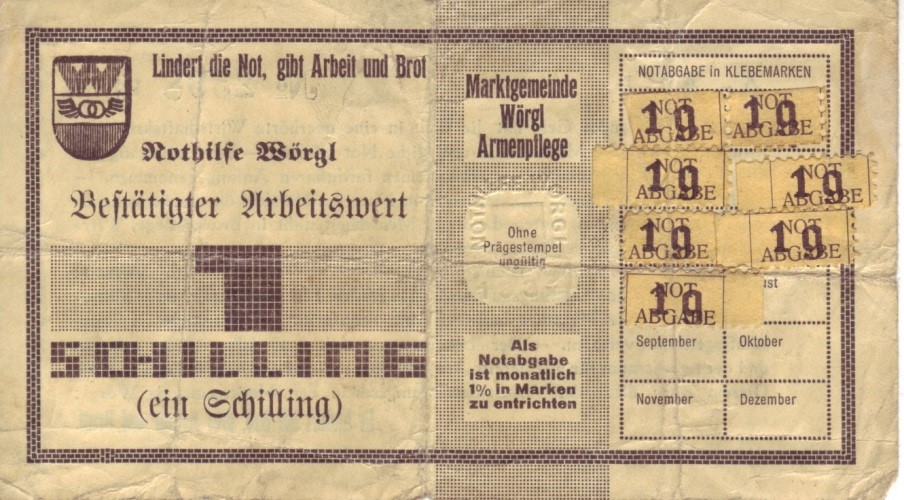

Actually, negative interest rates are not new

But the concept of negative interest rates is not a new one and dates back almost a century – also referred to as demurrage – with Silvio Gesell credited as being the original advocate. The method of implementing negative interest rates was rather novel. Taking a look first at “normal” interest bearing notes: an investor who historically bought these bonds or notes would receive a physical certificate with a series of coupons. To receive interest payments one would periodically clip off a physical coupon from the certificate and redeem it for the interest payment. In fact, the word “coupon” originates from a French word which means to “cut off”.

Negative nominal interest rates were implemented along similar lines, but with one change: the notes needed to be stamped. One would thus have to purchase a stamp at regular intervals in order to retain the value of the note: paying to hold the physical notes results in a tax on holding currency. Failure to have the note periodically stamped would render it void and worthless.

Example of Schilling note with demurrage and stamps from the 1930s

Source: Prescient Securities; Wikipedia

Two important changes over the last hundred years or so is the development of the global economy, and technological progress. The implementation of negative interest rates is now possible on a scale which was previously unimaginable. The vast amount of negative yielding debt outstanding is testament to advances and developments which enable previously identified concepts on a much grander scale. We have crossed the zero lower bound on interest rates and the use of new policy options are redefining the boundaries.

One would think that all our modern tools and developments would have been better able to assist us to understand and solve some of the current geopolitical frictions, financial market dynamics and economic challenges we are faced with. But the world is an increasingly complicated place. To make some sense of the debt and yield dynamics requires an understanding of macroeconomics, financial markets, regulatory trends and policy making frameworks.

How does SIM value bonds in these uncharted waters?

A good starting point is to look for investment opportunities that offer a good margin of safety, and keep a close eye on valuations and fundamentals as they change. It’s important to make a distinction between local and international bond valuations.

As is often the case in South Africa, our bond market runs counter-cyclical to most developed bond markets. In fact, SA long bonds are still offering among the highest local currency real yields in emerging markets. Sanlam Investment Management (SIM) is therefore overweight SA long bonds, as reflected in our flagship multi asset fund, the SIM Balanced Fund. Even if inflation settles at the top end of the 3% to 6% inflation target, a real return of 3% is on offer. This is particularly attractive given the low real returns available in equity markets, as well as global bond markets.

As far as SA inflation-linked bonds (ILBs) are concerned, the SA government is in effect in control of the rand printing press so the default risk on rand-denominated ILBs is low, as long as the inflation-linked component of the SA government’s total debt stays at a reasonably low level. Currently it is at 24%. There is probably more risk with the accuracy of the measurement and the measurement methodology of inflation, especially during periods of very high inflation or hyper-inflation. If this is a problem, then the inflation adjustment applied to these bonds would be compromised. We therefore still prefer SA conventional bonds to ILBs as is reflected in the position sizes of the SIM Balanced Fund.

Moving on to international bonds, even though global sovereign bond yields weakened after the election of Trump as president, we are keeping our underweight position. At a yield of about 2.4%, US long bonds offer a positive real return relative to our long-run inflation assumption of 2% for the developed world. We are concerned about long-run global inflation and would require an attractive premium above 2% before investing in developed market bonds.

All information and opinions provided are of a general nature and are not intended to address the circumstances of any particular individual or entity. We are not acting and do not purport to act in any way as an advisor or in a fiduciary capacity. No one should act upon such information or opinion without appropriate advice after a thorough examination of a particular situation. We endeavor to provide accurate and timely information but make no representation or warranty, express or implied, with respect to the correctness, accuracy or completeness of the information or opinions. Any representation or opinion is provided for information purposes only. Unit trusts are generally medium to long-term investments. Past performance of the investment in no guarantee of future returns. Unit trusts are traded at a ruling price and can engage in borrowing and scrip lending. Sanlam Investments consists of the following authorised Financial Services Providers: Sanlam Investment Management (Pty) Ltd (“SIM”), Sanlam Multi Manager International (Pty) Ltd (“SMMI”), Satrix Managers (RF) (Pty) Ltd, Graviton Wealth Management (Pty) Ltd (“GWM”), Graviton Financial Partners (Pty) Ltd (“GFP”), Radius Administrative Services (Pty) Ltd (“Radius”), Blue Ink Investments (Pty) Ltd (“Blue Ink”), Sanlam Capital Markets (Pty) Ltd (“SCM”), Sanlam Private Wealth (Pty) Ltd (“SPW”) and Sanlam Employee Benefits (Pty) Ltd (“SEB”), a division of Sanlam Life Insurance Limited; and has the following approved Management Companies under the Collective Investment Schemes Control Act: Sanlam Collective Investments (RF) (Pty) Ltd (“SCI”) and Satrix Managers (RF) (Pty) Ltd (“Satrix”). Although all reasonable steps have been taken to ensure the information in this document is accurate, Sanlam Collective Investments (RF) (Pty) Ltd (“Sanlam Collective Investments”) does not accept any responsibility for any claim, damages, loss or expense; however it arises, out of or in connection with the information. No member of Sanlam gives any representation, warranty or undertaking, nor accepts any responsibility or liability as to the accuracy of any of this information. The information to follow does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act. Use or rely on this information at your own risk. Independent professional financial advice should always be sought before making an investment decision. Sanlam Group is a full member of the Association for Savings and Investment SA (ASISA). Collective investment schemes are generally medium- to long-term investments. Please note that past performances are not necessarily an accurate determination of future performances, and that the value of investments may go down as well as up. A schedule of fees and charges and maximum commissions is available from the Manager, Sanlam Collective Investments, and a registered and approved Manager in Collective Investment Schemes in Securities. The maximum fund charges for the SIM Balanced Fund include (including VAT): An initial advice fee of 3.42%; initial manager fee of 0.00%; annual advice fee of 1.14% and annual manager fee of 1.25%. The most recent total expense ratio (TER) is 1.60%. Additional information of the proposed investment, including brochures, application forms and annual or quarterly reports, can be obtained from the Manager, free of charge. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Collective investments are calculated on a net asset value basis, which is the total market value of all assets in the portfolio including any income accruals and less any deductible expenses such as audit fees, brokerage and service fees. Actual investment performance of the portfolio and the investor will differ depending on the initial fees applicable, the actual investment date, and the date of reinvestment of income as well as dividend withholding tax. Forward pricing is used. The Manager does not provide any guarantee either with respect to the capital or the return of a portfolio. The performance of the portfolio depends on the underlying assets and variable market factors. Performance is based on NAV to NAV calculations with income reinvestments done on the ex-div date. Lump sum investment performances are quoted. The portfolio may invest in other unit trust portfolios which levy their own fees, and may result is a higher fee structure for our portfolio. All the portfolio options presented are approved collective investment schemes in terms of Collective Investment Schemes Control Act, No 45 of 2002. International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information. The Manager has the right to close any portfolios to new investors to manage them more efficiently in accordance with their mandates. The portfolio management of all the portfolios is outsourced to financial services providers authorized in terms of the Financial Advisory and Intermediary Services Act, 2002. Standard Bank of South Africa Ltd is the appointed trustee of the Sanlam Collective Investments Scheme.

Share On:

Comments are closed.