In cyberspace, no-one can hear you scream!

There are fortune tellers and powerful Sangomas out there who can address all your money problems, sort out delicate relationship issues, and even counter the evil eye. I perhaps missed the decolonised tertiary syllabus at varsity, but there is always an element of mysticism which grips the human spirit. It also is this penchant for the supernatural perhaps that often leads us to believe that not everything in the world comes with a rational explanation.

In the financial world, the label of bubbles gets attached to many difficult-to-explain phenomena but few have come close to the current euphoria surrounding crypto currencies. This prompted the highest paid banking CEO in the world, Jamie Dimon (CEO of JP Morgan Chase) to recently portend that he would fire anyone who trades in bitcoin or similar currencies.

In South Africa, we have witnessed a proliferation of Ponzi schemes with the latest MMM scheme being another high profile example of the old adage that if it’s too good to be true…it probably is. Nearly all Ponzi schemes have the same modus operandi: investors are promised eye-watering returns over short periods of time. Early investors tend to do well and word-of-mouth leads to a growing number of investors being suckered in, but the actual investment strategy underlying the scheme always remains very obscure. In the end, the pyramid collapses when the pay-outs to investors inevitably exceed the new investment proceeds, preventing the scheme from robbing Peter to pay Paul.

The first question is why so many of us believe in ‘get rich quick’ schemes. I guess this is the same reason we have a series of adverts, every January, ranging from medicinal remedies to exercise regimes, which claim to be able to get rid of our December over-indulgences effortlessly within weeks. While the majority of people will give up by March, there is always that one spectacular example of success, that unique someone who is prepared to testify to the validity of the formula – “I tried the fatkill remedy and I lost 20 pounds in 3 weeks!” Similarly in the financial world, there is nothing more convincing than an acquaintance claiming that they invested x and got 2x within a month. Who doesn’t want to look good? Who doesn’t want to get rich… quickly, effortlessly? Sign me up!

In the financial world, bubbles are always based on some shred of truth. Yes in a digital world, crypto currencies have a place. A medium of exchange, a currency accepted by major nations which can circumvent onerous financial regulation and be transacted securely – for now – and cheaply across borders, makes for an attractive alternative currency. The recent online fanfare that Pick n Pay was accepting bitcoin in its store proved a damp squib when the company clarified the fact that a pilot project had been on trial at its canteen store at its head office! In a world where Central Banks have printed over $10 trillion since the global financial crisis, there has been a growing distrust in fiat currencies. Well instead of trusting central bankers and governments who issue currency legally – you would have to place your faith in a complex web of computers. The bears have felt gold could be the answer, but then if the financial system is going to collapse, it’s pointless storing your gold booty in a bank safe. Enter crypto currencies – gold-like qualities but stored in ledgers safe from the doomsday of a global banking collapse. What’s not to like?

One of the key problems to bear in mind is that most crypto currencies are not regulated and are not legal tender per se in South Africa. Hence if you pay for a transaction using a crypto currency and the goods are never delivered, it is next to impossible to get the transaction reversed and even trace who the payment has gone to. In the cybersphere, no one can even hear you scream!

Starting off as ‘currencies’, digital currencies have become the favourite instruments of speculation. One of the key attributes of some crypto currencies – for instance, no more bitcoins will be produced after 2025 – has made them susceptible to a short squeeze by speculators, whereas other fiat currencies depreciate over time due to the constant printing of money.

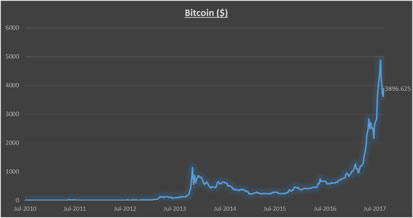

Perversely, the fear of rampant inflation caused by quantitative easing initiated by global central banks pushed many speculators to seek alternative currencies. However, the alternative is far from safe. The current bitcoin bubble is in fact one of the most extreme examples witnessed in current time. Over the past few decades, globally we’ve seen a number of bubbles: the global property bubble in the mid-90s, the dot com bubble, the silver bubble of 2001, etc. In nearly all of these cases, asset prices increased 1000% or more – the common trait is that it took at least a decade to inflate. In the case of Bitcoin, prices went up by over 1000% within a mere two years!

Source: Morningstar, August 2017

Just like at the peak of the financial crisis, financial engineers came up with derivatives of mortgage backed products – infamously known as CDO Squared. Now we have MMM trying to relaunch their Ponzi scheme in South Africa and elsewhere with bitcoin as its currency of choice! So while block chain technology is here to stay and has an increasingly wide range of applications, it is a case of buyer beware if you start believing that crypto currencies are a sure way to riches, rather than – at best – another transaction mechanism. The recent investment by Rand Merchant Investment in Luno, a bitcoin exchange, reminds me of the old adage that in the gold rush the people who got rich were the ones selling the shovels to the gold prospectors!

I may not be a Sangoma but I think I can help you with one financial matter – if you don’t want to become poor, don’t think of crypto currencies as the easy way to accumulate wealth. My first consultation is, by the way, free.

This publication is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act. Although all reasonable steps have been taken to ensure the information in this document is accurate, Sanlam Investments does not accept any responsibility for any claim, damages, loss or expense, however it arises, out of or in connection with the information in this document. Use or rely on this information at your own risk. Independent professional financial advice should always be sought before making an investment decision. No member of Sanlam gives any representation, warranty or undertaking, nor accepts any responsibility or liability as to the accuracy of any of this information. The contents of this document remains the property of Sanlam Investment Management (Pty) Ltd and may not be reproduced without the written permission of Sanlam Investment Management (Pty) Ltd.

Sanlam Investment Management (Proprietary) Limited is a Licensed Financial Services Provider. Sanlam is a full member of ASISA. Sanlam Collective Investments(RF) Pty Ltd., a registered and approved Manager in Collective Investment Schemes in Securities. Collective investment schemes are generally medium- to long-term investments. The Sanlam Investment Management (SIM) Balanced Fund is a multi-asset, high-equity fund and is exposed to equities, which means the prices will go up and down. The Retail class is the most expensive class offered by the Manager. The maximum fund charges include (including VAT): An initial advice fee of 3.42%; annual advice fee of 1.14% and annual manager fee of 1.25%. The most recent total expense ratio (TER) is 1.67%. The SIM Top Choice Equity Fund is a high conviction, pure equity fund. The fund is exposed to equities, which means the prices will go up and down. Sanlam Investment Management Top Choice Equity Fund aims to deliver above average growth of capital over the medium to long term. The fund may display high volatility in the short to medium term and is suitable for the sophisticated investor with an aggressive risk profile. The Retail class is the most expensive class offered by the Manager. Maximum fund charges include (incl VAT): Initial advice fee, 3.30%. Initial manager fee, 0.00%. Annual advice fee, 1.14%. Annual manager fee, 1.02%. Total expense ratio (TER), 1.19%. The SIM Enhanced Yield Fund is an interest-bearing fund that invests in a wide range of debt instruments. The Retail class is the most expensive class offered by the Manager. The maximum fund charges include (including VAT): An initial advice fee of 0.34%; annual advice fee of 1.14% and annual manager fee of 0.47%. The most recent total expense ratio (TER) is 0.49%.

Please note that past performances are not necessarily an accurate guide of future performances, and that the value of investments / collective investment units / unit trusts may go down as well as up. Commission may be paid and, if so, would be included with the brokerage charges, securities transfer tax, auditor’s fees, bank charges, trustee fees and levies in the overall costs, which will be levied against the fund. A schedule of fees and charges and maximum commissions is available from the manager, Sanlam Collective Investments(RF) Pty Ltd on request. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Collective investments are calculated on a net asset value basis, which is the total value of all assets in the portfolio including any income accrual and less any permissible deductions from the portfolio. Portfolio performance is calculated on a NAV to NAV basis and does not take any initial fees into account. An annualised growth rate is used for all performance data of 12 months or longer. Income is reinvested on the ex-dividend date. Total return performances are published. The source of performance data and risk statistics is Morningstar. Actual investment performance will differ based on the initial fees applicable, the actual investment date and the date of reinvestment of income. Forward pricing is used. The Manager does not provide any guarantee either with respect to the capital or the return of a portfolio. The manager has the right to close the portfolio to new investors in order to manager it more efficiently in accordance with its mandate. If the fund holds assets in foreign countries and could be exposed to the following risks regarding potential constraints on liquidity and the repatriation of funds, macroeconomic, political, foreign exchange, tax risks, settlement risks and potential limitations on the availability of market information. Derivatives are instruments generally used as an instrument to protect against risk (capital losses), but can also be used for speculative purposes. Examples are futures, options and swaps.

Share On:

Comments are closed.