Budget 2021: key points for investors

Minister Mboweni’s Budget speech on 24 February was short and – while not sweet if we consider the country’s growing debt – at least not more bitter for investors than last year. All investment-related taxes remain the same.

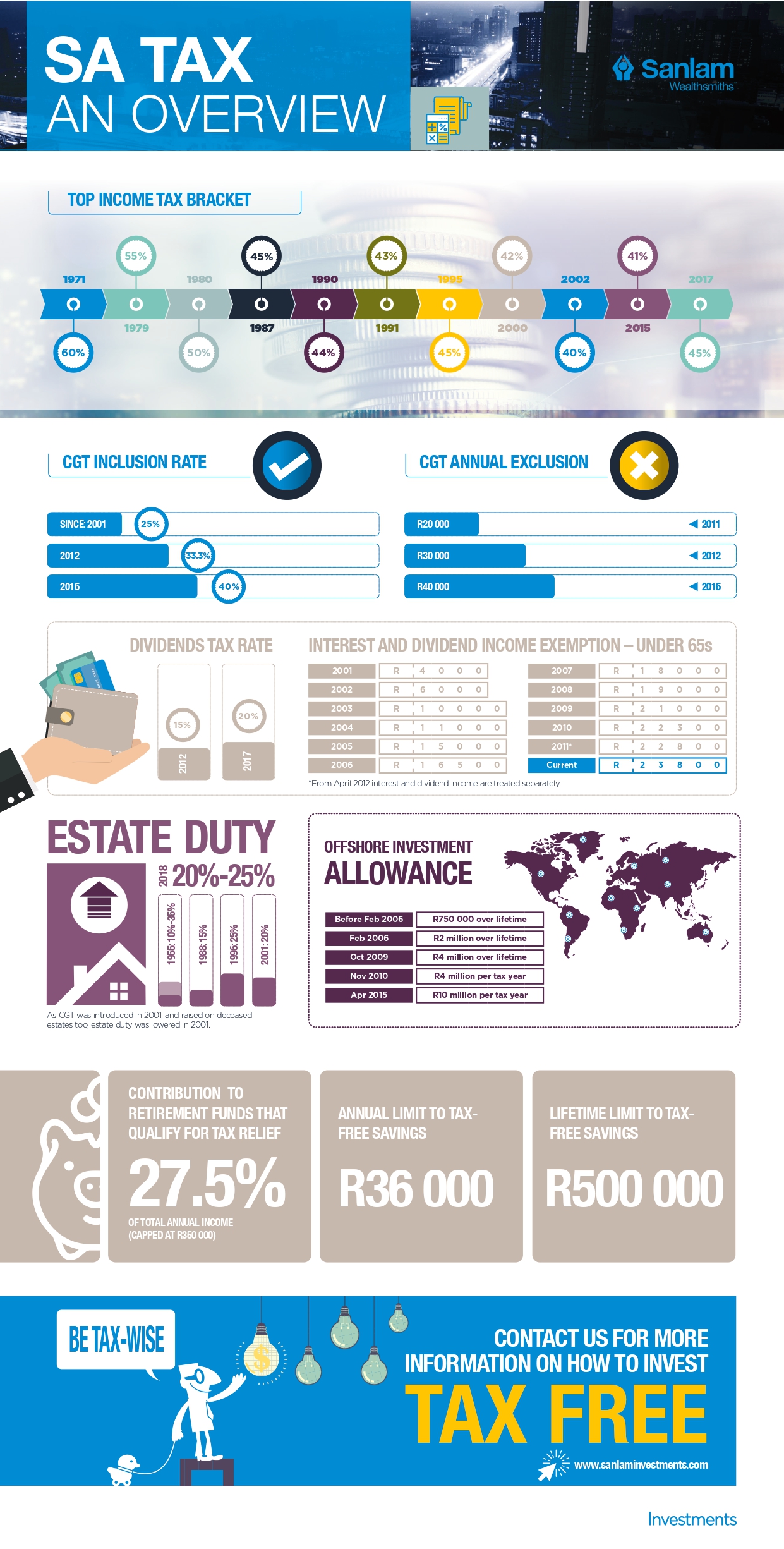

An uneventful Budget after steady tax hikes

The truth is an uneventful Budget belies decades of incremental tax hikes until we’ve reached the point where, in 2021, South Africans are keeping company with some of the most heavily taxed countries in the world.

As our ‘SA tax over the decades’ infographic shows, the following tax rates have increased over the past decade:

• Top marginal income tax rate (now 45%)

• Capital gains tax (CGT) inclusion rate (now 40%)

• Dividends withholding tax (now 20%)

• Top estate duty tier (now 25%)

At the same time the annual interest rate exemption has stayed constant at R23 800 for under 65s since 2012 and is unlikely to be raised again now that tax-free savings accounts have been introduced.

No wealth tax but we have CGT and estate duty

Rumours of a new wealth tax did not manifest. But it’s worth noting that CGT and estate duty are both taxes on wealth accumulation. Especially at death, the payment of both capital gains tax and estate duty on the estate of the deceased can be substantial after a lifetime of capital accumulation. Fortunately, retirement funds and living annuities are excluded from the estate when calculating both these taxes and therefore also carry tax benefits upon death.

Sin taxes are not a tax on investors

Considering the already high level of taxation, it’s encouraging that Treasury did not meddle with any of the existing taxes on investments. This year can therefore be seen as a victory for investors.

To boost investing in this country, raising taxes on consumption instead of investment is the way to go. Taxes on consumption include:

- VAT (but with ample zero-rated and exempt products)

- Sin taxes

- Fuel levies

VAT was raised to 15% only three years ago, so ‘sin’ taxes and the fuel levy were the only two remaining routes left for Minister Mboweni, and these he made use of.

You may soon be able to buy several annuities at retirement

While no changes were made to the tax tables at retirement or upon withdrawal from your retirement fund, Treasury is looking at proposals to provide retirees with more options when converting their retirement savings to an annuity on retirement. At their chosen retirement age, investors may take up to one-third of the value of a retirement fund in cash and the first R500 000 at retirement is taxed at 0%. With the remaining two-thirds, it’s currently possible to buy only one (life or living) annuity per retirement product. It is proposed that investors should be allowed to purchase more than one annuity from the compulsory two-thirds portion of a retirement fund, and allowed to do so from different annuity providers.

Our tax rates are high but remember the tax breaks

In the light of high tax rates, it is crucial for investors to make use of the two main tax-efficient investment vehicles, retirement funds and tax-free savings accounts (TFSAs). The annual contribution limit for TFSAs is still R36 000 per tax year and R500 000 over your lifetime. Any contribution above these limits will be taxed at 40%.

In addition, you can invest 27.5% of your total income (salary plus other income) in retirement products every tax year and receive tax relief from SARS on those contributions. The contributions which enjoy tax relief are capped at R350 000 per tax year.

Taxes are unavoidable, but Treasury is not blind to the important role that savers and investors play in the economy. TFSAs and retirement products are a sure way for investors to minimise tax, giving you a better chance at good net-of-tax investment returns over your lifetime.

Share On:

Comments are closed.