Blending risk factors/styles

Part 4/10: Blending risk factors/styles

Client level of adoption/allocation:

How to get the best out of factor investing

Not so long ago investment professionals vehemently debated which was best: active or passive management. Then the debate evolved into both sides acknowledging the role of the other, and the conversation moved on to how to blend active and passive in a portfolio. Now, with the advance in tools that are able to break down the risks to which both active and passive strategies expose the investor, the focus has shifted to how to blend the underlying risk factors (or styles such as value, quality, dividend yield and momentum) to build more diversified, risk-smart portfolios.

Factors are now considered to be the fundamental building blocks of investment returns. Understanding the different risk factors in your portfolio will lead to better insights and more informed portfolio construction decisions, says Jason Swartz, head of Portfolio Solutions at Satrix. As a result, what is now termed ‘factor investing’ is beginning to revolutionise the investment industry.

Factor-based strategies (or smart beta) exploit the returns that come from harvesting ‘factor premiums’ aka ‘risk premiums’. A common example of harvesting a risk premium is the so-called carry trade in foreign exchange investing, where investors take on inherent risk premia such as political and inflation risk across borders and are often well rewarded for doing so. But choosing the right factor strategy or combination to harvest the inherent risk premia is easier said than done.

Targeting these premiums optimally can significantly improve the risk-return profile of a portfolio. When you blend style factors that are not correlated it can help diversify portfolios, mitigate risk and enable your portfolio to generate a return premium above that of the broad market.

Blending single-factor portfolios has great value for investors who appreciate diversification among factors, as well as the transparency and predictability of performance between the factor building blocks,” says Swartz. These blended factor portfolios tend also to deliver higher risk-adjusted returns than the broad equity benchmarks, with a lower tracking error than most single-factor strategies.

Although many single-factor strategies have earned a premium above the market, each of these factors have also suffered periods of underperformance under certain market conditions, because of their innate cyclicality. As such, the risk of being exposed to a single factor is significant. For this reason, blending a number of uncorrelated factors produces more diversified portfolios. This blended portfolio mitigates the peculiarities associated with each individual factor and produces return outcomes that are substantially more reliable and predictable.

Figure 1: Three-year distribution of returns for Value versus a blend of Value, Quality and Momentum

Can you tactically adjust your factor allocations?

Can you tactically adjust your factor allocations?

One contentious position on blending factors is: do you tactically adjust your factor allocations to take advantage of cyclical performance, or do you employ static (fixed) allocations through time and rebalance periodically?

At Satrix, we have taken the latter view, arguing that timing factor performance is enormously challenging, and that the incremental impact of simply using static allocations will pay off over time. We do not discourage clients from employing factor timing – at the margin – based on either valuations or economic cycles. However, employing this approach would require a specific skills set and expertise. In our view, strategic allocations to specific factors better serve the requirements of a blended factor portfolio.

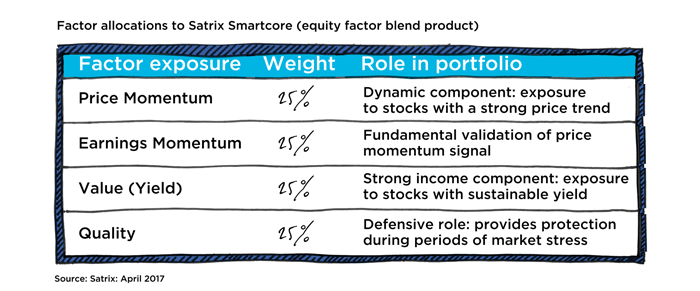

When blending single factors, you need to consider which factors are included in the blend. In the table below, we illustrate our house-view equity blend of domestic factors, which is made up of Satrix’s four single factor building blocks and weighs them equally.

Figure 2: Factor allocations to Satrix Smartcore (equity factor blend product)

Portfolios that blend factors display higher risk-adjusted returns than the broad equity benchmarks with a lower tracking error than most single-factor strategies. These portfolios offer great value for investors who are looking to maximise diversification amongst factors, and who appreciate the transparency and predictability of the difference in performance between the factor building blocks.

Share On:

Comments are closed.