April 2021 market overview

During April, the US Congress passed two large stimulus bills, which is expected to boost US government spending by about 13% of annual GDP. The increase may be too large, too soon, and lead to long-term inflation, but investors certainly showed no fear of inflation during the month. While more money is being printed, it’s not necessarily being spent – a significant portion is being saved by the average American. And for many those savings find a home in the stock market.

World’s largest economy shows recovery after stimulus cheques

The US data released during April contained plenty of good news. Retail sales did well on the back of stimulus cheques and vaccination progress, up 9.8% month-on-month to March. Initial claims for unemployment insurance dropped to the lowest level since the start of lockdown. And industrial production grew strongly.

Japan and the US strive for supply shift

Also during the month, Japanese Prime Minister Suga met with President Biden. The agenda? To discuss how these two giant economies could shift supply chains away from China. Among other things, the two leaders agreed to spend more on research and development, particularly relating to new generations of mobile telephony. This shift away from China could initially lead to cost inefficiencies and the IMF expressed concern around the negative impact this could potentially have on global GDP.

As one crypto exchange falls, another one goes public

With bitcoin slowly gaining traction as an alternative to fiat currencies, the original cryptocurrency reached a new record during April in the run-up to the public listing of the Coinbase exchange. In stark contrast to the global excitement, sentiment toward crypto exchanges was less exuberant locally as the first steps towards the liquidation of one of the oldest South African crypto exchanges, iCE3, were taken after pricing discrepancies were discovered.

Biggest block trade on record is imminent

Other big news was the announcement by Prosus (majority owned by Naspers) of its plans to sell a 2% holding in tech giant Tencent, worth about $15 billion, to institutional investors. This transaction, which would lower its Tencent stake to 28.9% could potentially be the biggest block trade on record ever.

Unlike many tech companies, which are thriving in the new stay-at-home pandemic world, South African banks are reflecting the embattled consumer. During April, Capitec, for example, reported that its net credit impairments rose 75% for the year to end February. Its net income dropped 9% for the period.

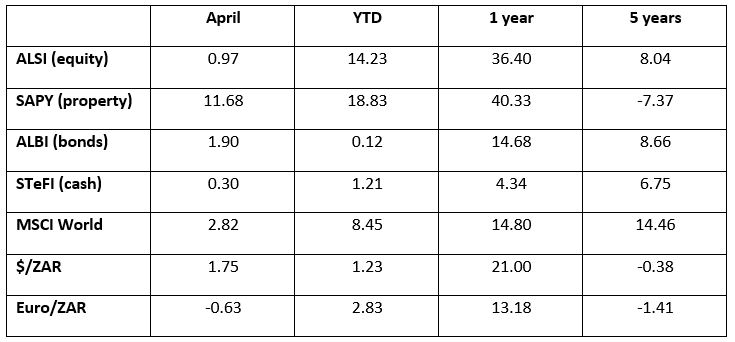

Don’t be fooled by property’s rise in April

It was hard not to notice the fast rise of the listed property sector in April, with the SAPY returning 11.68% for the month. But this is still part of its recovery from disappointing performance in preceding years. SA equities as measured by the FTSE/JSE All Share Index (ALSI) gave a total return of 0.97% for the month. The rand strengthened 1.75% against the US dollar but weakened 0.63% against the euro. The MSCI World index returned 2.82% in rand terms for the month. SA bonds (ALBI) gained 1.90% during the month and cash (STeFI) returned 0.30%.

The crash is hidden in the comeback of the past year

Over the past 12 months, most markets have made a strong comeback since hitting lows at the start of the pandemic. The ALSI returned 36% for the year to end April. Listed property is looking deceptively rewarding at 40.33% for the past year. The ALBI returned 14.68% for the year, and cash gave 4.34%. The rand strengthened 21.0% against the US dollar and 13.18% against the euro over the 12 months to end April. The MSCI World Index gave South African investors 14.8% in rand terms.

Over five years, world equity is the winner

Over the past five years to April 2021, the ALSI returned 8.04% per year. As the worst performer over this period, listed property (the SAPY) returned -7.37% annualised over the past five years. Bonds, as measured by the ALBI, at 8.66% returned more than local listed equities. Cash gave 6.75% p.a. on average over the past five years. The MSCI World Index (developed market equities) gave a 14.46% p.a. total return in rand terms over the past five years, comfortably beating all major SA asset classes. SA consumer inflation averaged 4.2% p.a.

Table 1: Total returns to 30 April 2021

Source: Morningstar | Total returns annualised to 30 April 2021

Share On:

Comments are closed.