A V-shaped recovery is the norm, not the exception

By Peter Urbani, head of Portfolio Construction at Sanlam Investments Multi-Management

There is heightened uncertainty around the impact that Covid-19 (worsened by the recent Moody’s downgrade on SA government bonds) is currently having on markets and explains the dramatic volatility in markets in recent weeks. Many experts had hoped for a ‘V-shaped’ recovery in the markets once quarantines were removed and spending and production resumed. This would imply a quick rebound to normality after a sharp fall. But the last few weeks have cast doubts on this, and there are fears of a far more protracted recovery in the form of a U-curve.

The economy and stock market often follow different recovery curves

It’s important to distinguish between the stock market and the economy when referring to recoveries. A disconnect between economic and market behaviour is quite common, and often in times of recession the market leads the recovery, while the economy is slower to follow. The research supporting this article is specific to the South African stock market.

What is a V-shaped recovery?

In equity markets, A V-shaped recovery is characterized by a sharp market sell-off followed by a quick and sustained recovery. Throughout history, there have been numerous such instances, including the more recent 2008 – 2009 Global Financial Crisis and the Great Depression of 1929. In each instance, history has shown that the recovery was a lot swifter, and twice as strong as initially anticipated.

What does history tell us?

We take a look back in history to 1925 and remind you that the unpredictability and volatility associated with market gyrations are perfectly normal. More to the point, historically stock markets have risen by far more than they’ve fallen, and the actual time taken to recoup the losses was – on average – twice as fast as expected. The message here is clear: if you sell your shares in a panic as they fall, you might miss out on the recovery as the markets rise again, effectively locking in your losses.

Using data from the JSE Total Returns Index since 1925, we see that the average of the ten worst drawdowns in history was a staggering -39.5%. For perspective, the current drawdown we’re experiencing is -21.72% (period for current drawdown is 30 May 2019 to 31 Mar 2020), and only ranks 13th in the 40 worst drawdown since 1925.

More importantly, the average return on the JSE in the 12 months following the bottom of the drawdown, was 33.7%. Effectively, this is more than double the average annual return of 14.5%.

The average actual recovery time is more than twice as fast as expected

From what we’ve seen through historical data, the average expected time to recover from all 40 drawdowns since 1925 was 24 months (two years). The actual time to recoup losses after a major drawdown was only nine months (under a year), effectively more than twice as fast as expected.

“The larger the drawdown, the more likely the recovery is V-shaped and twice as fast as expected”

The only exceptions to this were South Africa’s departure from the British Union in 1948 and the run up to World War II in 1939.

An additional interesting statistic reveals that the average compound annual growth rate (CAGR), a useful measure of growth over multiple time periods, in the five years following a drawdown, was 19.4%. This is almost 500 basis points more than the average under all conditions.

Let’s take a closer look at a few historically significant market crashes:

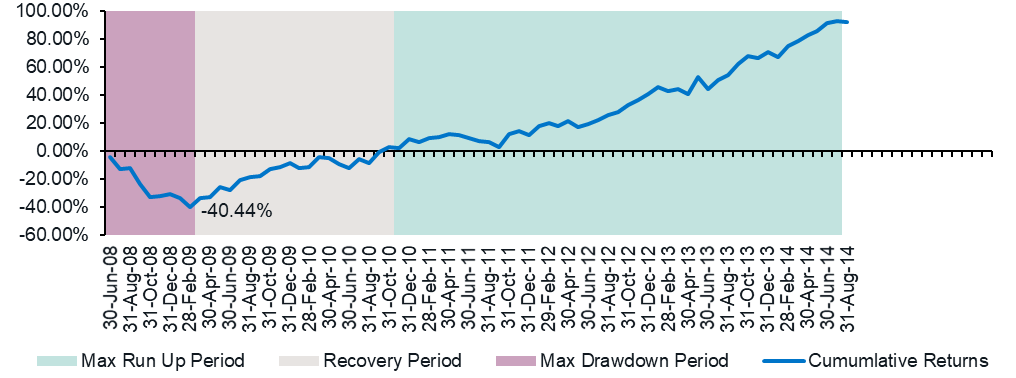

1. Global financial crisis:

Drawdowns on the JSE and recovery time: 30 June 2008 to 31 July 2014

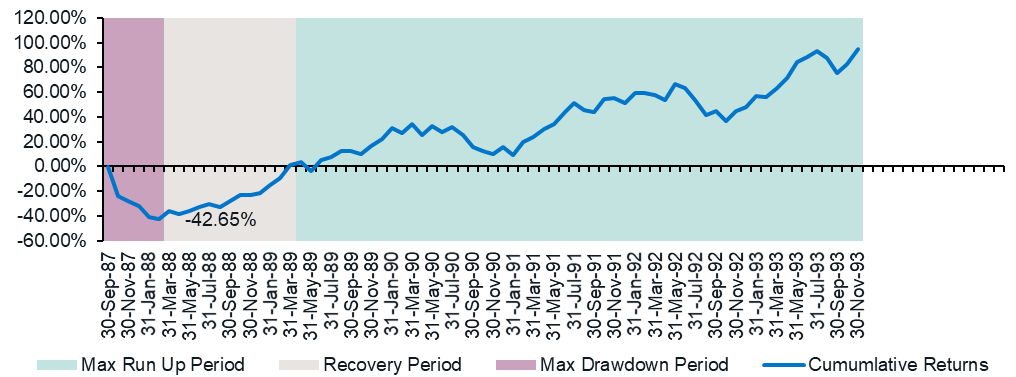

2. 1987 market crash (‘Black Monday’):

JSE drawdown and recovery time: 30 Sept 1987 – 30 Nov 1993

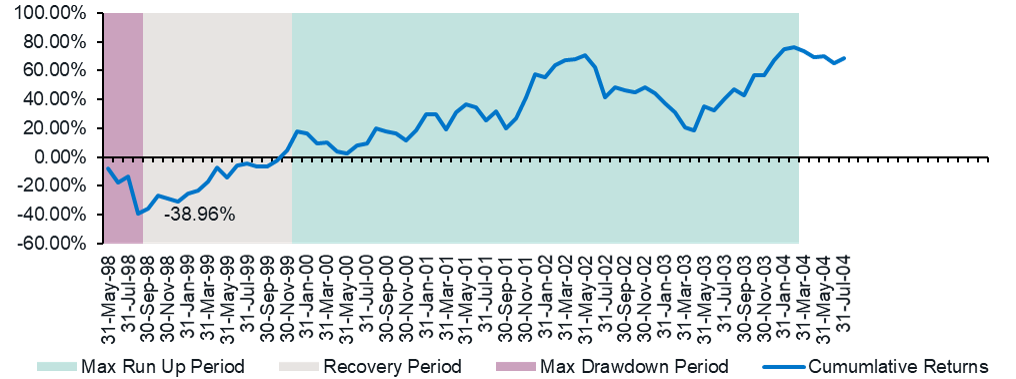

3. 1998 Russian debt default / Asian financial crisis:

JSE drawdown and recovery time: 31 May 1998 – 31 July 2004

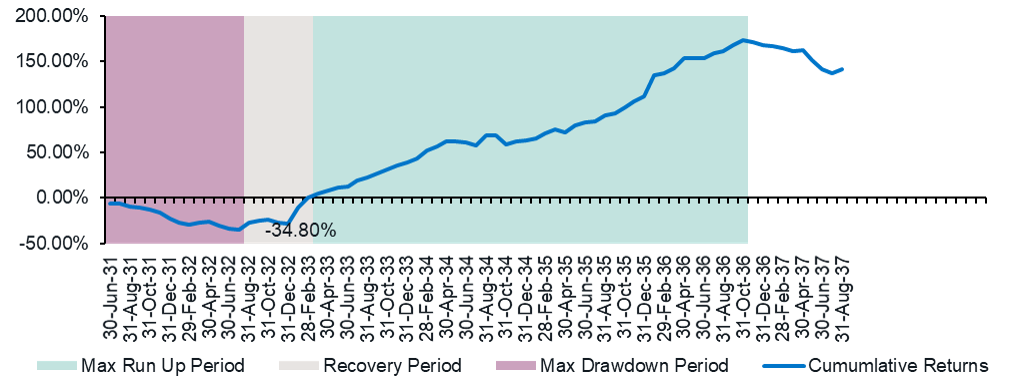

4. 1929 Great Depression:

JSE drawdown and recovery time: 30 June 1931 – 31 August 1937

What about our current market situation?

The required returns to recover from our current -21.72% drawdown is 27.8%. The expected time to recover would be between 1.43 to 1.95 years (17 to 23 months). However, based on the average actual rate ratio of 41% mentioned earlier in this article, a more realistic expected time to recover from the current drawdown would be seven to ten months. Much sooner than one might think.

This certainly gives one pause for thought, and once again reiterates the timeless wisdom that investors should not give in to fear or panic, and remain invested through market dips. Yes, markets do react severely to large, unexpected events, but history has shown that recovery may be quicker than expected.

We leave you with these thoughts:

• History has shown us that the recovery from market shocks can be swift.

• If you try to time the markets, you’re at risk of losing out from the recovery.

• Stay invested; the recovery may be swifter and far stronger than you expect.

Share On:

Comments are closed.