Choose the risk that’s right for you

Most people, when starting to save for the first time, simply deposit their money with their bank, either in a notice or fixed-term deposit. While this feels safe, there are still risks. The first one is the risk that the bank is put under curatorship – as happened to African Bank in 2014. Having all your eggs in one basket turns out quite painful in a scenario like this when your assets are frozen and most – if not all – of your interest is lost.

Secondly, putting the worst-case scenario of a bank failure aside, large bank deposits also carry the risk of your money not keeping up with inflation after tax, as interest earned is taxable along with your personal income. This is particularly true if you’ve grown a large deposit and your annual income places you in the 41% or 45% tax bracket.

To beat inflation, diversify your portfolio and grow wealth over the long term it’s necessary to also look at non-bank investments, such as unit trusts.

“How much interest do you offer?”

Coming from a background where your savings have always been with a bank, it’s understandable that the most common question asked by investors looking to take the leap to unit trusts is “How much interest do you offer?” Unlike bank deposits, though, unit trust funds do not offer a guaranteed interest rate. Instead they invest in underlying assets of which the prices go up and down. They take on this risk – called market risk – in an effort to deliver higher returns for investors than that of a bank deposit over the long term. The extent to which prices will go up and down is unknown at the start of the investment, and therefore it is impossible to say beforehand how much your investment will return.

“Could I have the maximum return, with no risk, please?”

Investor nirvana would be a place where you get the highest possible return with no risk. Unfortunately, investor nirvana does not exist. For starters, no form of saving or investment is entirely risk-free. And, secondly, there’s a direct relationship between the size of potential returns and the size of market risk that you need to take to achieve those returns. To achieve above-average returns, you need to be willing to face the risk of your investment value going both up and down at times.

“I don’t like risk. Is it really worth it?”

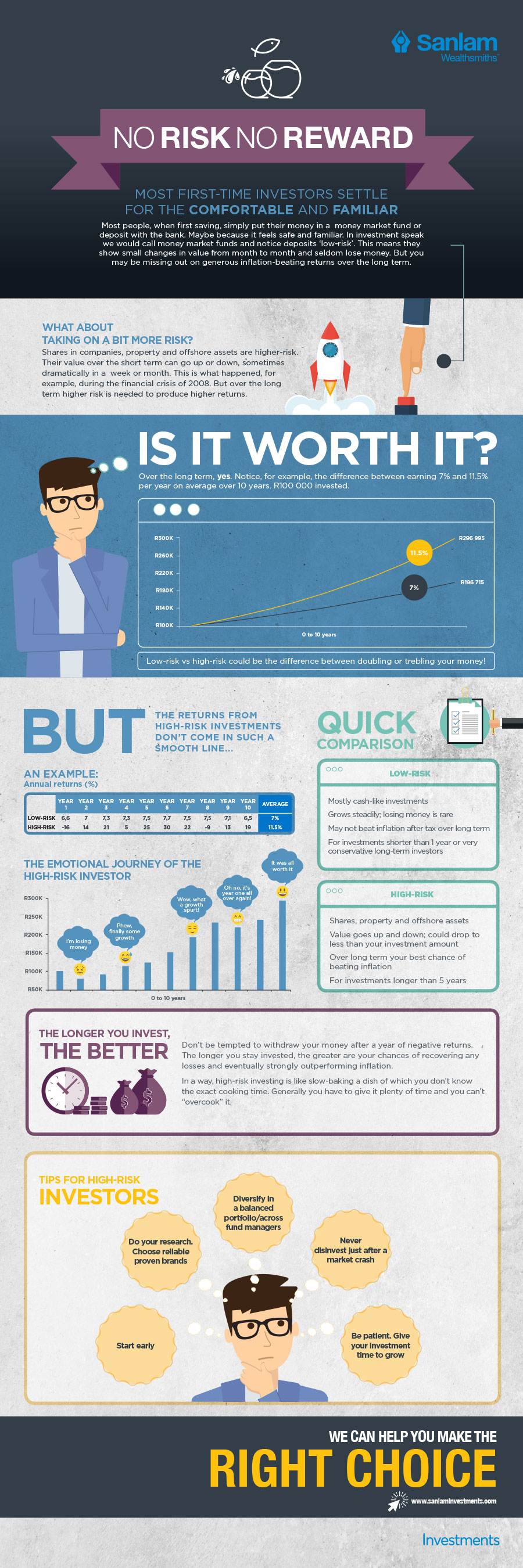

Yes, if you can commit to staying invested despite the emotional roller coaster ride of having your returns wiped out by a market crash over the short term, like we saw in 2018 when the local stock market dropped 8.5% and listed property delivered a shocking -25.3% in one year. Because over 10 years or more, the more volatile high-risk unit trusts generally deliver a significantly higher return than cash.

In our example on the infographic below we compared investing in cash at 7% per year vs investing in high-growth assets giving you potentially as much as 11.5% year on average. R100 000 invested at 7% at the start of 10 years comes to just under R200 000 at the end of the 10-year period; that same R100 000 can potentially grow to nearly R300 000 in high-growth assets. Over 10 years or more, whether you choose a bank deposit or a high-risk unit trust can mean the difference between doubling or trebling your money!

But taking on more market risk is not for everyone.

Be only as brave as you can afford to be

There are investors who cannot afford to take on much market risk, such as retirees or anyone else who is relying solely on their investment for a monthly income. It’s hard to absorb the shock of a market crash if you need to pay your bills from the income linked to your (suddenly diminished) investment value. If you identify with this group of investors, you might prefer the most stable form of unit trust – a money market fund. Or speak to your adviser to invest only a certain portion of your money in a balanced fund with a low allocation to shares/equity and listed property.

Prepare for your leap into the unknown

If you’re ready to take the leap and take on more risk – defined as uncertainty in returns – it’s a good idea to do more research before you invest and, also, to put a safety net in place.

Step 1: Find out your risk profile

Just as you need to find out which division you belong to before taking part in a sports tournament, you need to know which type of investor you are. Investors are normally classified as either conservative, cautious, moderate, moderately aggressive or aggressive – based on a combination of how much risk they can afford to take on and how much risk they feel comfortable with. If you only need the money far in the future, you are generally considered as someone who can afford to take on a lot of risk. However, you may not necessarily feel comfortable with risk, taking your risk profile down from aggressive to moderately aggressive or moderate.

Your financial adviser will take you through a comprehensive questionnaire to establish your risk profile, or you can try one of the many online risk profiling tools available.

Step 2: Do your fund research

If you have a financial adviser, he or she will be familiar with most of the more than 1 000 funds currently available to South African investors. A good financial adviser will know which ones have consistent track records and an investment philosophy and process that will suit your risk profile, and will be able to explain to you what to typically expect from a manager in different cycles of the market.

If you’re investing without a financial adviser, you’ll need to tackle the research yourself. You can start by finding out which funds offered by the large, trusted brands match your risk profile. Then get hold of the fund fact sheets or MDDs (new terminology) of all the funds that you are considering. Pay particular attention to the lowest annual return figure on the MDD. This is the worst return the fund has ever delivered over any one-year period since it was launched. Would you be comfortable with this low level of return? Most investors combine two or three unit trusts from different fund managers to safeguard themselves in case one of the funds has a particularly bad year.

Step 3: Set up an emergency fund

Similar to a long-distance athlete preparing for a race by making sure he or she has enough water and emergency snacks, you need to create a safety net for yourself separate from your unit trust investment. Just as you wouldn’t want to exit a race to visit a shop for emergency supplies, you also need to make sure that you don’t ever have to withdraw money from your unit trust while the race for rewarding returns is still on. An emergency can hit at any time; it doesn’t wait until markets have run strongly. And the last thing you want is to find yourself in a position where you have to withdraw money from your unit trust shortly after a market crash. Therefore, always have separate savings in a 24-hour notice deposit for emergency expenses like car repairs or medical bills.

Once you’re in it, remember the rules of the game

Once you’ve chosen your unit trust funds and invested, you’re in it for the long haul. Cautious investors, who normally choose a combination of money market and other interest-yielding unit trusts, need to invest for a minimum of two years to see good returns; moderate investors need at least three years; moderately aggressive investors at least five years and aggressive investors at least seven years. The returns are often “lumpy,” with years of almost no or negative growth following years of strong growth. Patience is rule number one of long-term investing.

The moment you start taking on more risk than a bank deposit, there will be years that your money “grows backwards” and years when it seems like your investment is standing still. Which brings us to rule number two: never withdraw money straight after a market cash; in fact, this is a good time to invest more, as asset prices are low and you get more units per cent you spend. A good financial adviser will also act as a coach to keep you focused on your long-term goals and make sure you stay the course.

As with any other risk you might have taken in your life so far, such as changing jobs, cities, or even countries, or starting your own business, you can increase your chances of success by doing the research, preparing yourself well and sitting it out when initially you may face some ups and downs. You’ll spot us in the crowd cheering you on as you take the first step to notch up your investment risk. May the reward over the long term be worth the potholes you may have to navigate in the short term.

[/vc_column_text][/vc_column][/vc_row]

[/vc_column_text][/vc_column][/vc_row]

Share On:

Comments are closed.