Building sophisticated multi-factor portfolios

Part 8/10: Building sophisticated multi-factor portfolios

Client level of adoption/allocation:

Earlier, in Part 4 of this series, we discussed the diversification benefits of allocating strategic weights to single factor strategies. In that exercise we were simply ‘blending’ factors – essentially combining single factors on a sub-portfolio basis.

At Satrix, we take the view that the incremental impact of simply using static allocations – as opposed to tactical allocations – will pay off over time. We do not discourage clients from employing factor timing based on either valuations or economic cycles. However, employing this approach would require a specific skills set and expertise. In our view, strategic allocations to specific factors serve the requirements of a blended factor portfolio better than tactical allocation.

Apart from the blended factor portfolio approach, another approach to combining factors would be multi-factor portfolio construction. This approach first aggregates factor rankings on a stock level, and then builds a portfolio based on this overall factor score. Let’s look at the advantages of multi-factor portfolio construction compared to a simple blend of factor portfolios.

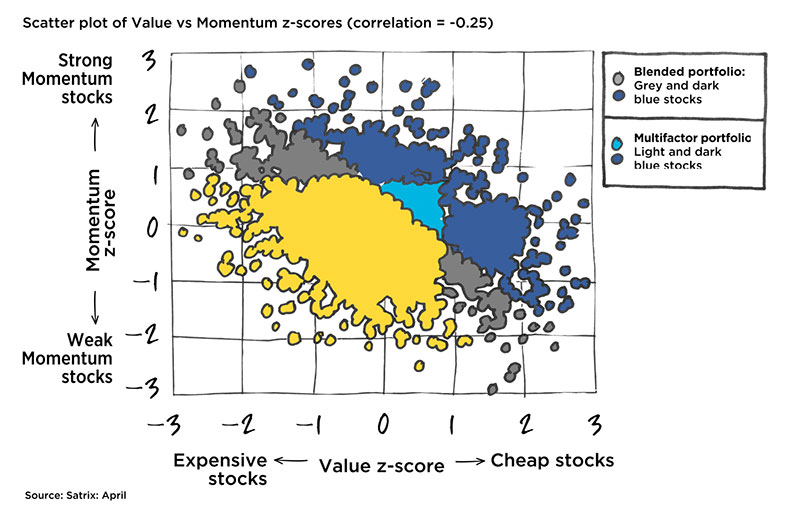

The first advantage of a multi-factor approach compared to the blended portfolio approach, is that a multi-factor approach improves the transfer of information by finding stocks with reasonably positive exposures to multiple factors rather than stocks with very strong exposures that may simultaneously have very poor exposures to another factor (see Figure 1).

Figure 1: Scatter plot of Value vs Momentum z-scores (correlation = -0.25)

Selected Factors

Another advantage using a multi-factor approach would be trading efficiencies. By not having to execute separately managed single factor portfolios, turnover is reduced by netting offsetting trades against each other.

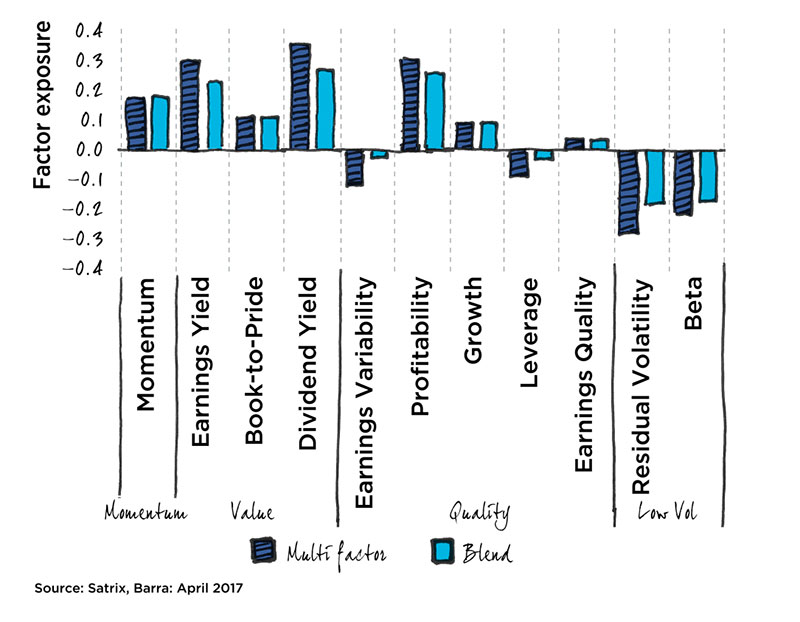

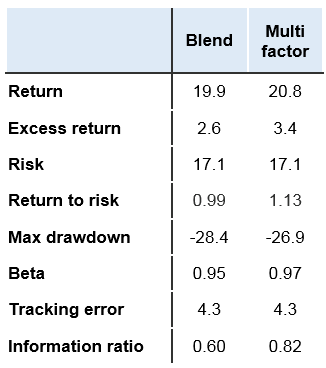

We decided to empirically test a multi-factor approach in South Africa in order to assess the extent of the improvement in efficiencies versus a blended approach. The results both in overall factor exposures (Figure 2) and risk-adjusted performance since 2001 (Figure 3) are positive. The enhanced factor exposures versus the blended portfolio illustrates the stronger reflection of intended factors, as opposed to a blended approach where exposures may be watered down given opposing factor scores in sub-portfolios.

| Figure 2: Average factor exposures of multi-factor versus blended portfolios (2001 to 2016)

|

Figure 3: Back-tested factor portfolio results (2001 to 2016)

|

We will, however, note that multi-factor benefits depend on a few considerations, including how correlated underlying factors are to each other, the number of factors used as well as the tracking error applied to the multi-factor portfolio.

Ultimately, the value of multi-factor portfolio construction is improved factor efficiency and enhanced risk-adjusted returns. Despite this benefit, blending single factors into a portfolio has value and application to clients who prioritise transparency of portfolio attribution and flexibility in allocating between factors.

For more information on this topic or further details on our analysis, please feel free to contact us directly or visit our website.

Share On:

Comments are closed.