Tactical factor tilts

Part 6/10: Tactical factor tilts

Client level of adoption/allocation:

There are typically two frameworks that one can use to inform tactical investment decisions around factors. The first is based on fundamental information, drawing on relative valuations and/or price momentum. The second approach, which we outline in this article, uses economic cycles to inform the short- to medium-term prospective returns of factors.We consider the latter to be more intuitive and objective.

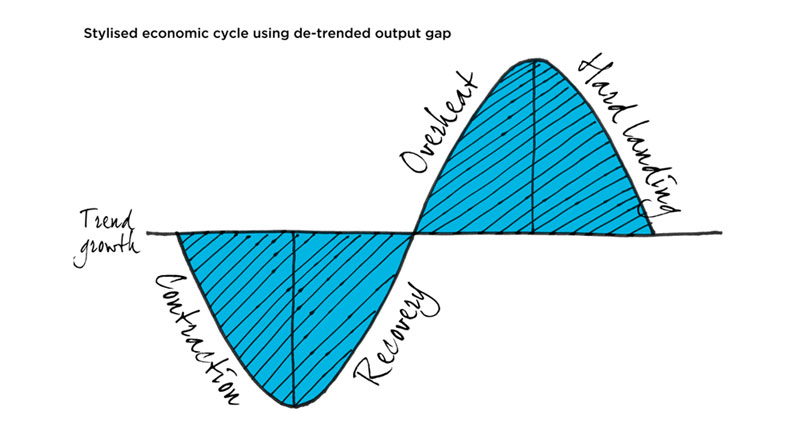

We used an output gap[1] as an economic cyclical indicator, and divided this indicator into four distinct and successive phases depending on the direction of the indicator, as well as whether the indicator was above or below economic trend growth. Our aim is to understand how each factor behaves during various economic cycles, and use this framework as a basis to tactically shift portfolio factor exposures.

Figure 1: Stylised economic cycle using de-trended output gap

[1] We used the SA Manufacturing PMI as a proxy for economic activity, and applied a Hodrick–Prescott (HP) filter over the raw data to express the business cycle around a dynamic trend.[/fusion_text][fusion_text]Our results are fairly intuitive, and summarised in Figure 2 below. We not only highlight which single factors performed best and worst, but which blend of factors is optimally suited to each cycle.

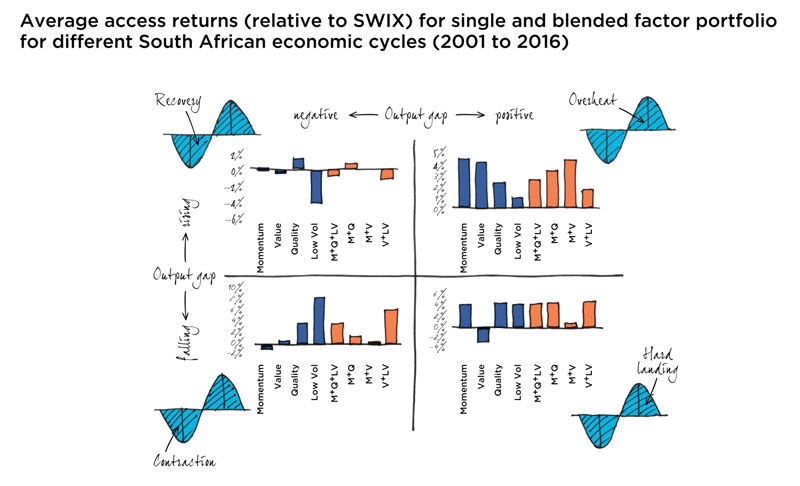

Figure 2: Average excess returns (relative to SWIX) for single and blended factor portfolios for different South African economic cycles (2001 to 2016)

During the Contraction phase of an economic cycle, growth slows down and equities typically do poorly versus bonds (as interest rates are being cut in this phase). It makes sense that Low Volatility and Quality strategies are successful as investors look for defensive-orientated shares. As the economy transitions to Recovery and interest rate cuts take effect, equities tend to perform well versus bonds. But because the market is still cautious, Quality is preferred to Low Volatility. Thereafter, as the economy gains traction and shifts into Overheat, investors move into Value and Momentum, which represent the more cyclical equity strategies. Lastly, during the Hard Landing phase, a more diversified blend of factor portfolios tends to perform well, with the market starting to position itself for a defensive turn.

When using an ‘economic cycle’ approach to tactically allocate between factor exposures it’s important to be aware of the risks of such an approach. Firstly, it’s not guaranteed that the historical relationship remains intact. Secondly, getting the timing of the next economic cycle right is tricky.

For more information on this topic or further details on our analysis, please feel free to contact us directly or visit our website.

Share On:

Comments are closed.