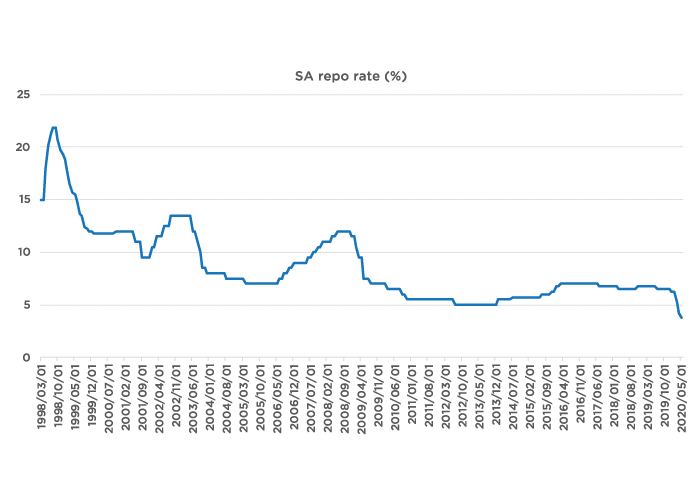

SA policy rate reaches record low

On Thursday, 21 May the South African Reserve Bank cut the repo rate by 50 basis points – in line with general market expectations as well as our own expectation. This brings the repo rate to its lowest point on record.

Source: IRESS

Drastic monetary policy measures in line with rest of the world

The Reserve Bank’s decision to cut interest rates and to implement measures to increase liquidity in the market is not unique to South Africa. Other leading central banks around the world have implemented aggressive measures to minimize the adverse effects of COVID-19 on their respective economies. For example, already in March the US Federal Reserve Bank slashed the federal funds rate to near zero and expanded its balance sheet by purchasing a range of assets.

As South Africa continues to contend with the effects of COVID-19, various interventions will be required in order to support the country’s already fragile economy. The governor of the Reserve Bank, Lesetja Kganyago, further cautioned that monetary policy on its own is not sufficient and that other prudent macroeconomic policies and structural reforms would be required in order to cushion and revive the South African economy. Moreover, the country’s GDP forecast has been revised downwards and CPI lower, and risks are still assessed to be downside. The Reserve Bank revised its GDP forecast to a deeper contraction at -7.0% for 2020, compared to the previously forecast -6.1%.

At the beginning of May 2020, the SA government partially relaxed the five weeks of hard lockdown and permitted some businesses to operate in addition to essential services. However, the South African economy may take longer to recover because phase 4 of the lockdown still excludes many activities. As a result, reduced business activity and low inflation rates pave the way for further rate cuts in the future.

On the day of the Reserve Bank’s decision to cut the repo rate to 3.75% the rand strengthened against the US dollar, a positive reaction perhaps but it’s also noteworthy to remember that the rand was particularly weak and potentially quite oversold.

Effect on SIM’s fixed interest portfolios

From a portfolio point of view, we had already seen the local interest rate market rally significantly (i.e. trade stronger) in anticipation of the interest rate cut. This – and material market strength so far during the second quarter – benefitted our fixed interest funds’ performance in the short term. However, there is a downside to all the rate cuts: the inverse relationships between the yield and price of a fixed interest instrument. When interest rates decrease, the price of the instrument increases, which leads to an increase in value or a shorter-term profit. But, in fact, it decreases the forward-looking return prospects or yield of the instrument.

This is also true on a fund level. For our funds, such as the SIM Enhanced Yield Fund and SIM Active Income fund, we have thus seen very strong performance come through so far during the second quarter on the back of decreasing interest rates and the anticipation of decreases in the policy rate. This benefits the recent total return of our investors, but decreases the running yield going forward. In particular for clients who are withdrawing an income, it decreases the overall income the fund can deliver going forward.

It’s the inflation-adjusted returns that really matter

It’s important to remember that we are in a very soft inflation environment. At least clients can take comfort in the fact that the historic and current inflation-adjusted returns are still looking good and are in positive territory. Interestingly, our positive yield environment locally is in contrast to the global environment where we have seen negative yields become more prevalent. This has been causing a problem for not only savers but also for the global economy with many unintended consequences and unanswered questions about the wider implications of negative rates. The lower yields currently available locally at the ‘shorter end of the curve’, i.e. the repo rate, now make products such as the SIM Enhanced Yield Fund and the SIM Active Income Fund even more important. For our investors in these funds, we continue to work hard to seek out instruments with a high yield.

Disclaimer: All information and opinions provided are of a general nature and are not intended to address the circumstances of any particular individual or entity. We are not acting and do not purport to act in any way as an advisor or in a fiduciary capacity. No one should act upon such information or opinion without appropriate advice after a thorough examination of a particular situation. We endeavor to provide accurate and timely information but make no representation or warranty, express or implied, with respect to the correctness, accuracy or completeness of the information or opinions. Any representation or opinion is provided for information purposes only. Unit trusts are generally medium to long-term investments. Past performance of the investment in no guarantee of future returns. Unit trusts are traded at a ruling price and can engage in borrowing and scrip lending. Sanlam Investments consists of the following authorised Financial Services Providers: Sanlam Investment Management (Pty) Ltd (“SIM”), Sanlam Multi Manager International (Pty) Ltd (“SMMI”), Satrix Managers (RF) (Pty) Ltd, Graviton Wealth Management (Pty) Ltd (“GWM”), Graviton Financial Partners (Pty) Ltd (“GFP”), Satrix Investments (Pty) Ltd, Blue Ink Investments (Pty) Ltd (“Blue Ink”), Sanlam Capital Markets (Pty) Ltd (“SCM”), Sanlam Private Wealth (Pty) Ltd (“SPW”) and Sanlam Employee Benefits (Pty) Ltd (“SEB”), a division of Sanlam Life Insurance Limited; and has the following approved Management Companies under the Collective Investment Schemes Control Act: Sanlam Collective Investments (RF) (Pty) Ltd (“SCI”) and Satrix Managers (RF) (Pty) Ltd (“Satrix”). Although all reasonable steps have been taken to ensure the information in this document is accurate, Sanlam Collective Investments (RF) (Pty) Ltd (“Sanlam Collective Investments”) does not accept any responsibility for any claim, damages, loss or expense; however it arises, out of or in connection with the information. No member of Sanlam gives any representation, warranty or undertaking, nor accepts any responsibility or liability as to the accuracy of any of this information. The information to follow does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act. Use or rely on this information at your own risk. Independent professional financial advice should always be sought before making an investment decision. Sanlam Group is a full member of the Association for Savings and Investment SA (ASISA). Collective investment schemes are generally medium- to long-term investments. Please note that past performances are not necessarily an accurate determination of future performances, and that the value of investments may go down as well as up. A schedule of fees and charges and maximum commissions is available from the Manager, Sanlam Collective Investments, and a registered and approved Manager in Collective Investment Schemes in Securities. The maximum fund charges for the SIM Enhanced Yield Fund include (including VAT): An initial advice fee of 0.34%; annual advice fee of 1.15% and annual manager fee of 0.48%. The most recent total expense ratio (TER) is 0.49%. The yield on the SIM Enhanced Yield Fund is a current yield (6.32% at 31 Mar 2020) and is calculated daily. Income funds derive their income from interest-bearing instruments, which are any assets, such as a corporate or government bond, stock or money market instrument that pays regular, periodic interest to the investor. The maximum fund charges for the SIM Active Income Fund include (including VAT): An initial advice fee of 1.15%; annual advice fee of 1.15% and annual manager fee of 0.92%. The most recent total expense ratio (TER) is 0.93%. Additional information of the proposed investment, including brochures, application forms and annual or quarterly reports, can be obtained from the Manager, free of charge. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Collective investments are calculated on a net asset value basis, which is the total market value of all assets in the portfolio including any income accruals and less any deductible expenses such as audit fees, brokerage and service fees. Actual investment performance of the portfolio and the investor will differ depending on the initial fees applicable, the actual investment date, and the date of reinvestment of income as well as dividend withholding tax. Forward pricing is used. The Manager does not provide any guarantee either with respect to the capital or the return of a portfolio. The performance of the portfolio depends on the underlying assets and variable market factors. Performance is based on NAV to NAV calculations with income reinvestments done on the ex-div date. Lump sum investment performances are quoted. The portfolio may invest in other unit trust portfolios which levy their own fees, and may result is a higher fee structure for our portfolio. All the portfolio options presented are approved collective investment schemes in terms of Collective Investment Schemes Control Act, No 45 of 2002. International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information. The Manager has the right to close any portfolios to new investors to manage them more efficiently in accordance with their mandates. The portfolio management of all the portfolios is outsourced to financial services providers authorized in terms of the Financial Advisory and Intermediary Services Act, 2002. Standard Bank of South Africa Ltd is the appointed trustee of the Sanlam Collective Investments Scheme.

Share On:

Comments are closed.